A new journal paper co-authored by Professor Homayoon Beigi of Columbia Electrical Engineering and Mechanical Engineering and recent IEOR graduate Boris Ter-Avanesov showcases the power of artificial intelligence in the world of financial modeling. The study, titled “MLP, XGBoost, KAN, TDNN, and LSTM-GRU Hybrid RNN with Attention for SPX & NDX European Call Option Pricing,” was published in the May 2025 issue of the Journal of Mathematical Finance.

The 70-page paper marks the culmination of over three years of research and explores the performance of a wide range of AI models—including multilayer perceptrons (MLP), Kolmogorov-Arnold networks (KAN), and attention-enhanced hybrid RNNs combining LSTM and GRU units—for pricing European-style call options. The models were trained on S&P 500 and NASDAQ 100 index option data from 2015 to 2023, using real-world datasets with various levels of market volatility and maturity periods.

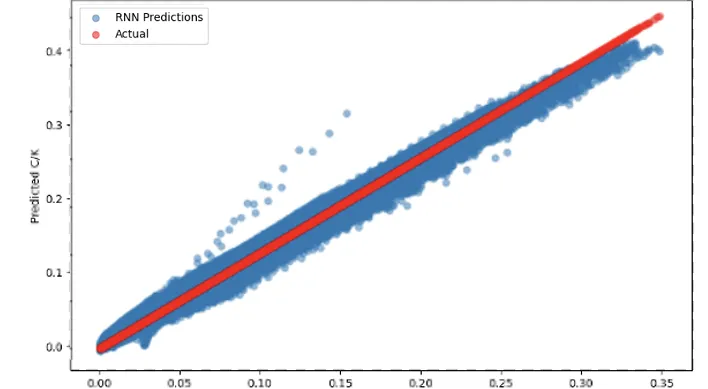

The study evaluates a series of machine learning and deep learning models—including multilayer perceptrons (MLP), gradient-boosted trees (XGBoost), Kolmogorov-Arnold networks (KAN), time-delay neural networks (TDNN), and a custom-built hybrid RNN that combines LSTM and GRU units with attention mechanisms—to predict the prices of European call options based on real historical market data.

Using data from 3.8 million SPX and NDX index option contracts between 2015 and 2023, the team trained and tested each model on input features such as strike price, time to maturity, risk-free rate, and six different rolling-window historical volatility estimates. The performance of each model was compared to the widely used Black-Scholes (BS) model, a benchmark in finance known for its simplifying assumptions but widely criticized for its inability to match real market behavior.

Their findings were striking: every machine learning model in the study outperformed the Black-Scholes benchmark. Among them, the best-performing model was the attention-based LSTM-GRU hybrid recurrent neural network (RNN), which captured complex temporal relationships and market dynamics that the BS model failed to account for. The study also showed that the Kolmogorov-Arnold network (KAN), inspired by the Kolmogorov-Arnold Representation Theorem, outperformed traditional feedforward networks in this context.

The study not only offers strong empirical evidence for machine learning's superiority over traditional pricing models but also introduces a rigorous framework for evaluating AI-driven option pricing tools.

📄 Read the full paper: https://www.scirp.org/pdf/jmf_1491180.pdf